Solo 401(k) plans, also known as Individual Solo(k) or one-participant plans, are a powerful retirement tool for entrepreneurs, offering unique advantages for business owners and the self-employed. Additionally, if the plan is self-directed or a Roth Solo 401(k) it offers tremendous investment flexibility because you have much more control over investment options and strategy.

In this quick reference guide, we'll address common questions surrounding Solo 401(k) plans, providing clarity on eligibility, establishment, contribution amounts, investment options, and more. We know time is money, but we want you to make informed decisions, so we’ll keep it short.

What is a Solo 401(k)?

A Solo 401(k) is a retirement plan designed for entrepreneurs, including independent contractors and self-employed small business owners. It applies to various business structures or entities, such as sole proprietorships, LLCs, C Corps, or S Corps.

Eligibility Restrictions

To qualify for a Solo 401(k), your business cannot have employees. The only plan participants are the business owner(s) and spouse employed by the business.

Establishment Timeframe

With the necessary information, you can establish or transfer your Solo 401(k) in minutes using our online platform.

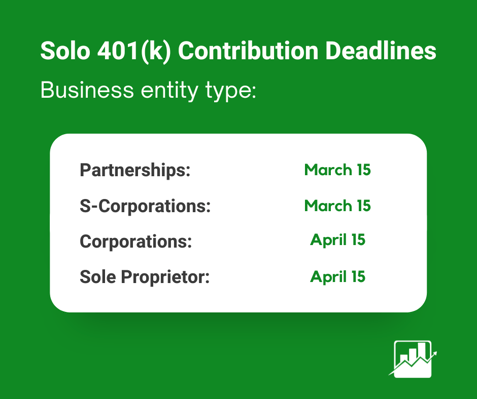

Deadline for Solo 401(k) Plan Establishment and Contributions

Previously, you had to open your Solo 401(k) by December 31st to make contributions for the current year. However, Secure 2.0 has extended the deadline. Now, you can establish a Solo 401(k) plan after the end of the year and before your tax filing due date. Therefore, in 2026, you can still open a Solo 401(k) and make contributions for 2025. See the deadlines below for your type of business entity.

EIN Requirement

To maintain accurate records and facilitate tax reporting, it is essential to obtain an Employer Identification Number (EIN) for your Solo 401(k). By having a distinct EIN for your Solo 401(k), the IRS will recognize that the income is specifically allocated to your retirement plan, rather than your business. This EIN is separate from the one you use for administrative and legal purposes related to your business.

Rollover Possibilities

You can rollover funds from other qualified plans into your Solo 401(k), including 401(k)s from previous employers, Traditional IRAs, and other eligible plans.

Spousal Participation

If your spouse works for the business, they can participate in the same Solo 401(k) plan, with their contribution limits determined by income, salary, and age.

Employee Presence and Full-Time Employees

If you have employees who are not owners you are not eligible for a Solo 401(k) plan. An alternative plan for employers with employees who are not owners is the SEP or SIMPLE IRA.

Plan Document Requirement

For an employer to establish a plan, the IRS requires that a Solo 401(k) have a written plan document. The most common documents used by employers to establish a plan are called prototype documents which consist of an Adoption Agreement and Basic Plan Document.

Annual Contribution Limits

For those under 50, the total combination of both employer profit-sharing contribution and employee salary deferral is $70,000 for 2025 and $72,000 for 2026. If an employee contributes the maximum employee deferral of $23,500 (2025) and $24,500 (2026) they can make an additional catch-up contribution of $7,500 (2025) or $8,000 (2026) if they are age 50 and older. Starting in 2025 and 2026, those aged 60 to 63 are eligible for a higher catch-up contribution limit of $11,250.The catch-up contribution can exceed $70,000 for 2025 and $72,000 for 2026. The maximum profit-sharing contribution is up to 25% of each eligible employee’s compensation.

Minimum Required Contribution

Solo 401(k) contributions are not mandatory, allowing flexibility in choosing whether to make yearly contributions.

Profit-Sharing Contribution Limits

Employer profit-sharing contributions are capped at 25% of income, not to exceed $70,000 (2025) and $72,000 (2026).

Participant Loans

Solo 401(k) allows participant loans from their own account. The maximum loan amount is up to 50% of the participant’s account balance with a maximum of $50,000.

Mortgage Loans for Solo 401(k)

One major advantage of Solo 401(k) is the option for a participant to borrow money from their account under the plan. If it's to be used to purchase a primary residence the loan could extend to 30 years, unlike the 5-year limit which 401(k) loans are limited to. The loan is still limited to 50% of the participants balance not to exceed $50,000.

Investment Options

A self-directed Solo 401(k) allows diverse investment options, including real estate, cryptocurrencies, private investments, and more.

Reporting Requirements

No annual tax reporting is applicable until assets exceed $250,000. The IRS Form 5500-EZ must be filed once this threshold is reached.

Checking Account Necessity

A checking account for your self-directed Solo 401(k) is required for receiving contributions, making investments, and to hold cash under the plan.

Multiple Accounts for Roth and Pre-Tax Contributions

Different contribution types must be tracked separately due to the different tax treatment and distribution timing for each type of contribution source (pre-tax deferrals, Roth deferrals, profit sharing, rollovers, and after-tax)

Solo 401(k) vs. IRA Costs

Solo 401(k) plans tend to have higher costs compared to IRAs due to the unique features, plan document requirements, and recordkeeping platform. However, these additional expenses come with benefits such as increased flexibility and compliance. Fees can vary depending on the services and software provided by the plan provider.

Unrelated Debt Financed Income (UDFI)

Solo 401(k) plans that use nonrecourse loans to purchase investments such as real estate are exempt from UDFI, making them advantageous for leveraging investments.

Form 5500-EZ Filing

Form 5500-EZ is filed annually when the Solo 401(k) plan balance exceeds $250,000 or upon plan termination, regardless of value. Our recordkeeping platform helps you do this reporting easily.

Understanding terminology and the rules of Solo 401(k) plans is crucial for entrepreneurs seeking a tailored retirement strategy. Whether you're navigating eligibility, annual contributions, or investment options, a Solo 401(k) can provide a robust solution for securing your financial future as a business owner. Schedule a free consultation to learn more about this wealth-building platform for solopreneurs.

Comments (0)