The current life expectancy rates continue to increase annually. The current life expectancy for U.S. in 2024 is 79.25 years, a 0.18% increase from 2023. We are living longer into retirement and finding the appropriate, low-cost IRA option to save for retirement is very important.

IRAs can complement federal benefits programs like Social Security. These social programs can help cover essential expenses that include monthly housing payments, grocery bills, and insurance premiums. What about personal income to do the things you love, or get a haircut?

You can use Individual Retirement Accounts (IRAs) to finance leisure activities. Examples include vacations, dining out, or taking up a new hobby. You can ensure your golden years remain blissful beyond Wednesday’s senior discount days. Let’s explore some options.

Laying the Foundation: Social Security and Retirement Planning

While Social Security offers a solid foundation for retirement, it may not cover all your needs. Many retirees find their income falls within the range of "floor" expenses, which are essential costs like housing, food, and utilities. These expenses can range from half to three-quarters of your total retirement income.

Social Security itself boasts several advantages. Payments arrive regularly, are guaranteed for life, and adjust for inflation to protect your purchasing power. Plus, they benefit from lower federal taxes and often exemption from state taxes.

However, the average Social Security benefit of $1,767 per month translates to just $21,204 annually. This can be a challenge, especially considering the poverty level for seniors. Additionally, while Medicare helps with healthcare, it doesn't cover everything.

Government programs like Medicaid, food stamps, and SSI exist to assist those below the poverty line. These programs ensure basic needs are met, but they may not provide the desired quality of life.

This is where strategic planning comes in. By exploring low cost IRAs and investments you understand, you can build upon the foundation of Social Security and create a more secure financial future.

Some important questions to consider are:

Can social programs cover the Alaskan cruise you've been dreaming of? Or a family reunion, wedding, or graduation?

Could there be any major or unexpected expenses not covered by a home equity loan, Social Security, or Medicare? If so, how can we prepare for them?

What about global economic crises, like the 2008 Great Recession, that many accounts never recovered from? As you can see, strategic retirement planning is essential to the future of your finances. Finding a low-cost strategy to prepare for life events — the good and the bad — matters when securing your financial freedom.

Low-Fee Retirement Plan Options

An IRA is a great way to save for retirement at a low cost. These accounts are all tax-advantaged and can help you save for retirement by growing the assets held in the account. There are several options depending on if you are self-employed or a W-2 employee.

The best way to learn about these options is to expand your financial literacy to then build your investment portfolio. That’s why investing in an IRA with low fees is crucial to building wealth for your retirement strategy. Why pay for IRA management fees if you don't have to.

Common Retirement Plans For Individuals

If you have a workplace retirement plan like a 401(k), you can set up a Traditional IRA or Roth IRA to make additional savings toward retirement. Common investments in these accounts can include CDs, savings bonds, individual stocks, ETF options, bonds, and mutual funds.

Traditional IRA

For 2024, Traditional IRAs allow you to make contributions up to $7,000 annually or $8,000 if you are 50 or older and would like to make catch-up contributions. Contributions to these retirement accounts are tax-deductible and your money grows tax-deferred. Taxes are collected when withdrawals are made from this account type.

Roth IRA

A Roth IRA also has tax-advantaged benefits. But, unlike a conventional or Traditional IRA, contributions are not tax deductible. The advantage of this is that it allows for tax-free withdrawals in retirement. This account type may work best for investors who think they’ll be in a higher tax bracket at retirement age.

The Roth IRA has income limits that determine your eligibility to contribute and the amount you can contribute each year. These limits are set by the IRS and apply to your modified adjusted gross income (MAGI).

Solo 401(k) Plans, SEP, and SIMPLE

Solo 401(k)s were created for business owners without employees. The plan can, however, cover the business owner(s) and their spouse. These plans offer self-direction and higher contribution limits. This makes them ideal for large real estate transactions or other larger investments.

SIMPLE and SEP IRAs offer business owners and the self-employed another chance to save for retirement. These accounts provide an excellent opportunity to plan for the future. If you have employees, these accounts may be an option.

Benefits of Self-Directed Account

Self-directed IRAs are a great option for investors with expertise a particular asset or those that want more access to alternative assets. As an investor, you get to find, pick, and choose investments that you want in your IRA. These types of accounts are not for hands-off investors.

The accounts mentioned above can be self-directed and hold alternative investments. Knowing what to look for can also help you save when comparing different financial institutions, the types of accounts they offer, and their associated fees.

A true self-directed retirement account is different from your traditional brokerage account that limits you to stocks, bonds, and mutual funds. For example, a "self-directed IRA" at Charles Schwab will not allow you to invest in real estate. This investment strategy can produce higher returns compared to brokerage accounts that commonly hold the traditional assets referenced.

In fact, many types of assets can be held in an IRA. However, many larger brokerages are not willing to allow clients to truly diversify their retirement portfolio in alternative investments outside the stock market.

Tips to Save More, Faster.

Contribute What You Can, As Early as You Can

It’s never too late to start a savings plan for retirement. The sooner, the better! Retirement security isn't about starting big; it's about starting smart. Even small, consistent contributions can snowball into a significant nest egg over time. This could be the difference between retiring earlier with financial security or retiring at any age with financial insecurity.

Real Estate IRAs

Real Estate IRAs, are self-directed IRAs that hold real estate assets. These accounts are another great way to save for retirement, especially if you know the market well.

There are many strategies to invest in real estate with IRA funds. Direct purchasing is the most common or popular method for this investment type. For smaller IRAs, partnering, leveraging, and opening a Checkbook control IRA LLC are investment options available.

Investment options include single-family rental units, multi-family properties, commercial properties, mortgage notes, land, international properties, or tax liens.

A real estate IRA shares the same rules as all other IRAs. For example, a real estate investment in an IRA cannot benefit you or your spouse, directly or indirectly before retirement. Also, you cannot claim losses in your income tax return.

The investment is treated like any other investment in an IRA. See our IRS rules and regulations on disqualified persons and prohibited transactions.

Get Help From An Advisor

A financial advisor can help you devise a strategy to build your wealth sustainably. They can help you understand how to meet your financial goals and keep you on track. Alternatively, they can also let you know if your portfolio isn’t performing well and how to improve it.

You can also research and find educational resources online. The IRS has a lot of educational tools on retirement plans for individuals and small businesses.

Beware of Fees

Fees can eat into your retirement portfolio growth, preventing you from reaching your retirement goals. High expense ratios can gradually consume your hard-earned retirement savings. Always do your due diligence by comparing fees before choosing your IRA custodian or provider.

Custodial Fees

Custodial fees may be paid yearly or monthly to the custodian or provider for maintaining the account. These can include administration fees, special asset fees, transaction fees, service fees, etc. Essentially, these are the fees charged to maintain your account.

IRA Transaction Fees

Transaction fees are typically charged each time you buy or sell an asset in your retirement account. Transaction fees vary depending on the service provided and can include wire transfers, establishing the account, or the purchase, sale, or exchange of an asset. Depending on how frequently you transact, these can add up quickly.

All Inclusive Fees

Every little fee adds up. Be aware of hidden fees such as annuity fees, rollover fees, commission fees and mutual fund expense ratios, and "all inclusive" fees. Always read the terms and conditions in the fine print to be vigilant that these fees won’t drain your account. Ask for an IRA fee schedule and review carefully.

Lastly, beware of rock-bottom fees. While a low fee IRA is attractive, it might come with trade-offs. Research the provider's customer service reputation. Striking a balance between reasonable, low fee IRA and quality service is key.

Let IRAR Help You

Sometimes, taking the first step is the hardest step. Finding your perfect low-fee retirement plan can start with a simple consultation. We aim to empower investors to build wealth through alternative investments at a lower cost.

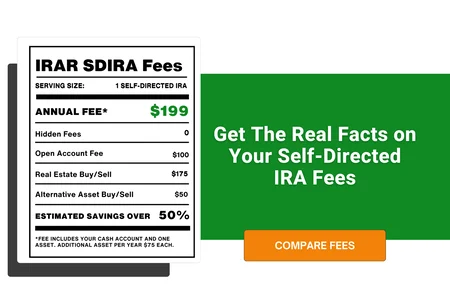

We have a low fee IRA structure that can help you save up to 50% compared to other self-directed IRA custodians. Our annual fee is per asset and not based on the value of your account. All accounts are self-directed.

Let us help you find a better, less expensive way to save for retirement without sacrificing the quality of service. Give us a call at 888-322-6534.

Comments (0)