Fees have a big impact on retirement accounts, they slowly add up over time, preventing you from putting your hard-saved money to work for your retirement. To help you make the most of your money, we’ve compiled a guide to these fees. After all, if you’re doing some of the work with self-direction, you shouldn’t have to overpay for your IRA.

Investing in real estate through a self-directed IRA as an alternative to traditional assets like, bonds, and stocks is a popular strategy for a robust retirement portfolio. Holding properties in a self-directed IRA provides greater diversification with tax-advantaged earning potential.

There are several key benefits to holding real estate in an IRA. Investors can generate rental income that goes back to the IRA tax-deferred. This not only grows the IRA but over time, the property value can also appreciate. This allows the investor to make more investments with these funds.

Like any other IRA, your self-directed IRA operates in a tax-deferred environment. This means that you do not pay taxes on the income earned from real estate investments held in your retirement account.

With a Traditional IRA, that means the real estate income won’t be taxed until withdrawals from the account are made at retirement age. Alternatively, Roth IRAs function using after-tax dollars. So assets withdrawn from a self-directed Roth IRA are tax-free.

Real estate as an asset has the potential to generate significant growth over time. Additionally, real estate investments can provide a hedge against inflation. That’s because real estate investments are not correlated with fixed-income or equity investments.

Nearly all real estate investment types that can be held in self-directed IRAs. These include undeveloped land, single- and multi-family rental homes, commercial real estate, private funds, and real estate development firms to name a few.

Still, investors will want to be mindful of the rules governing real estate held in a self-directed IRA. The two major rules set by the IRS: no self-dealing or working with disqualified persons and no prohibited transactions. For example, you cannot buy a property you already own from yourself or from certain relatives.

For any fixer-upper properties or other home repairs, the investor cannot work on the property themselves. An independent person with no stake in the game must maintain and repair the property.

Expenses for the property cannot be covered with personal funds. Instead, the IRA must pay all expenses related to the property. Investors will want to make sure their IRA can accommodate routine maintenance costs, property taxes, or unexpected major capital expenditures should the need to pay for them arise.

Furthermore, while owning real estate in an IRA will defer taxes on rental income, you are also prohibited from deducting losses, depreciation, or any other tax write-offs. Your IRA is already in a tax-deferred environment. This means that income is not being taxed.

Lastly, withdrawals for required minimum distributions (RMDs) from your real estate IRA must begin at age 70 and a half. Investors should ensure that the IRA has enough liquid assets to satisfy those withdrawals, in addition to the value of any real estate retained within it.

How to Get Started Investing in a Real Estate IRA

Self-directed IRA holders have to be able to draw on their own business savvy and resourcefulness. That’s one reason realtors make ideal candidates for holding property in a real estate IRA— they know the market well. However, working with experienced professionals can differentiate the investment process for all kinds of investors. Here’s who to work with to help you choose the right property:

- Real estate agents can assist in locating potentially lucrative investment properties.

- Non-recourse lenders can help you pursue non-recourse loans to afford the investment property if your retirement account doesn’t hold sufficient funds to purchase it.

- Financial advisors and accountants can come up with a cash flow analysis to aid in estimating the possible return on investment.

- Most importantly, investors should choose a real estate IRA custodian who is knowledgeable about fees that will not impede the account’s growth potential. Working with an asset based fee custodian is a lot more beneficial for the investor.

Self-Directed IRA Custodian

A knowledgeable custodian or IRA company will specialize in the administration and custodial care of non-publicly traded investments, such as real estate. Seasoned retirement account custodians can help streamline the real estate investment process. This is important when trying to meet funding deadlines.

The custodian will also be in charge of monitoring transactions and record-keeping of your assets. It is their duty to report IRA balances to the IRS annually.

Self-Directed Real Estate IRA Fees

Fees for a real estate IRA can vary depending on the custodian and the types of investments in the IRA. Sometimes this can also vary depending on the kind of self-directed IRA. Some custodians charge IRA fees based on a percentage of the account’s total value. That means, the larger the value of the assets, the more expensive the fees of the account.

In other cases, some custodians charge different fees based on the asset in the account. For instance, a Roth IRA that holds precious metals, may not have the same fees as one that has checkbook control. Understanding self directed IRA fee schedules or fee structures to calculate your IRA cost and annual fees is important. You can compare custodian fees by using this template.

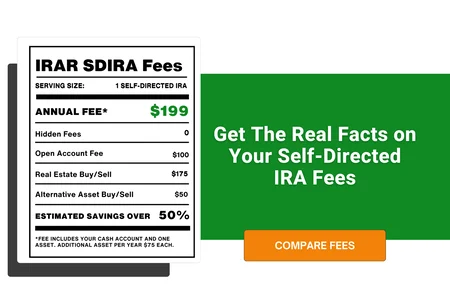

At IRA Resources, the minimum yearly account record keeping fee applies to all asset types. It doesn’t matter if you hold real estate or private placements, whatever your asset may be— the fees are the same. The flat annual fee is $199 for the first asset, with any additional assets $75 per asset. We do not have a separate fee for cash. Some providers do charge an asset fee for cash, or they incorporate the cash into the overall value of the account when billing.

IRA Resources Annual Fee |

|

|---|---|

|

Cash Only |

$199 |

|

Cash + 1 Asset |

$199 |

|

Cash + 2 Assets |

$274 |

|

Cash + 3 Assets |

$349 |

The annual fee covers filings and reporting to the IRS, custody of account, check deposits, issuance of statements, etc. But most importantly, as a client of IRA Resources, your annual fee gives you access to our client obsessed team. Not only does our team have a passion for the client experience, but our team members are well versed in real estate IRAs and the industry as a whole. On average, our employees have 8.5 years’ experience in the industry— wow! We know Real Estate IRAs!

Transactions Fees are the fees that are incurred for making a transaction. For example: when purchasing an asset, selling an asset, notary service, research and special services, wire transfers, checks, etc. Here is a complete list of our fees. We like to keep it simple and cost effective for our clients whenever possible, and that includes our fees.

Relevant: How to Avoid the Worst Kinds of Self-Directed IRAs

Real Estate IRA Purchase Fees

At IRA Resources, real estate purchases are $175. This fee includes processing of the earnest money deposit and non-recourse loan if you have one. Other providers may have additional charges for processing these. There are also transaction fees, depending on how the monies are sent to fund the sent to fund the investment, and whether overnight delivery of documents is required. investment, and whether overnight delivery of documents is required.

Fees Associated with a

|

|

|

Purchase |

$175 |

|

Check |

$10.00 |

|

Cashier’s Check |

$30.00 |

|

Overnight Delivery |

$30.00 |

|

Wire Transfer |

$30.00 |

|

ACH Transfer |

No Fee |

|

Notary Fee |

$15 |

If your real estate investment has mortgage payments, HOA fees, utilities and other fees, there is no fee for processing these payments. However, there are fees to deliver these payments via wire or check, as listed above. These fees are often consolidated by using a property manager (who pays the individual bills, with a flat fee deducted from the income of the asset before the funds are sent to IRAR for deposit), or bulk scheduling of payments in advance. We aim to help you save on fees in any way possible, so that your money goes where you intended— to your retirement account. Compare our fees and see for yourself.

If you’d like a more detailed breakdown of our fees, you can find them on our self-directed IRA fees page, along with information about our services. Or you can pick up the phone and give us a call— we’d love to hear from you, 888-322-6534.

Comments (2)