Real estate investors often compare two paths inside a self-directed IRA, buying property outright or using financing to help complete the purchase. When financing is involved, the loan must be structured as non-recourse, meaning the IRA, not the investor personally, is responsible for the debt. That distinction matters to both the IRA and the investor. This makes the loan structure an important part of understanding IRA-owned real estate.

A non-recourse loan may allow a self-directed IRA to purchase real estate without using only cash from the account. But it’s not the only thing to consider. The property fundamentals, account balance, income potential, ongoing expenses, and available IRA cash all deserve a closer look first.

Start with the investment plan, not the loan

A non-recourse loan may allow an IRA to purchase a property it could not buy entirely with cash, or to preserve funds for, repairs, insurance, taxes, or future investments. Financing is one option investors may consider, but the property should be evaluated based on income potential, expenses, reserves, and long-term objectives before deciding whether a loan is appropriate.

Why non-recourse structure matters in an IRA

A self-directed IRA is separate from the investor for ownership and tax purposes, so the rules around IRA-owned real estate are strict. With a non-recourse loan, the investor does not personally guarantee the debt and the property itself serves as the collateral. This structure is required because the IRA owner cannot personally pledge personal assets or otherwise extend credit to the IRA.

Those rules extend to how the property operates day to day. Rent goes back to the IRA, and property expenses are paid by the IRA. The IRA owner cannot personally pay bills, use the property, or guarantee the loan. Actions like these are classified as prohibited transactions, which include any improper use of an IRA by the owner, a beneficiary, or a disqualified person. A prohibited transaction can have serious consequences, including disqualification of the entire account

When investors may consider non-recourse financing

Non-recourse financing may fit when the IRA has a clear real estate strategy, and the investment can support the added responsibility of debt.

Investors may consider it when:

- The IRA does not have enough cash to purchase the property outright

-

The investor wants to keep IRA cash available for property-related expenses

- The investor is comparing financing with an all-cash purchase

Financing creates flexibility, but it is one option investors may consider as part of their overall investment plan. The decision may depend on the property’s income potential, projected expenses, reserves, vacancy assumptions, and the investor’s long-term goals.

What role a lender plays in a non-recourse loan

A non-recourse lender has its own underwriting process before approving a loan to the IRA. The lender may review the property, income potential, expenses, loan terms, available IRA cash, and reserves.

That review is separate from the investor’s decision. The lender is deciding whether the property and IRA qualify for financing.

Account liquidity still matters

When financing is involved, investors may also need to understand how much cash will remain in the IRA after closing.

Real estate investments need room to operate. Repairs happen, tenants move out, insurance costs fluctuate, and property taxes can increase. Because IRA-owned property expenses must be paid by the IRA, the account needs available cash after closing, not just enough to close.

A common mistake is treating the loan as a liquid solution. It may preserve cash at purchase, but the account still needs reserves to cover ongoing costs. Investors should ask whether the IRA can handle six to twelve months of expenses, vacancies, or unexpected repairs.

Debt can change the tax picture

When an IRA uses financing to purchase income-producing real estate, part of the income tied to the financed portion may be considered UDFI, unrelated debt-financed income. UDFI may trigger UBIT, or unrelated business income tax.

This is one reason the loan structure should be reviewed before the IRA closes on the property. Financing may help the account purchase an asset it otherwise couldn't, but it can affect how rental income and future gains are taxed.

UDFI and UBIT may affect the tax picture, but the possibility of paying these taxes does not automatically mean financing should be ruled out. Investors should understand how the taxes may apply and review the potential impact with a qualified tax professional.

The Rise of Real Estate in Retirement Accounts Industry Report

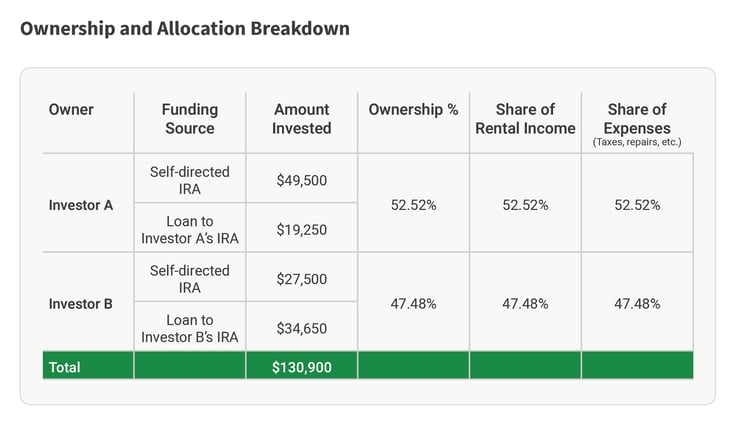

Here is a real-world example of how IRA cash and non-recourse loan proceeds can be used together in a single real estate purchase.

How IRAR can help

Non-recourse loans are one-way investors may finance real estate in a self-directed IRA. When financing is involved, investors may need to consider the property, account balance, income potential, expenses, reserves, and tax implications as part of the overall investment strategy.

IRAR helps investors understand how self-directed IRA real estate transactions are structured, including how IRA-owned property is titled, how expenses are handled, and what to consider before bringing financing into the account.

For investors who are ready to explore real estate inside a self-directed IRA, IRAR is a good place to start. Whether that means opening an account, reviewing an existing strategy, or simply learning more about how the process works, IRAR can help investors take the next step with a clearer picture of what is involved.

Comments (0)